Private credit is entering a new phase. Not because returns are disappearing, but because liquidity, timing and capital control matter more than ever.

For more than a decade, the asset class benefited from near-zero interest rates, excess liquidity, and a relentless hunt for yield. Institutional investors dramatically scaled up their allocations, attracted by contractual cash flows, downside protection, and illiquidity premiums of 200–400 bps over public debt. Against this backdrop, global private credit assets under management grew from approximately $500bn in 2015 to $3.5 trillion in 20251.

This environment has now fundamentally changed.

Higher for longer rates, increased dispersion of returns, tighter liquidity conditions and prolonged exit timelines are reshaping how Limited Partners approach private credit allocation. The central question for institutional investors is no longer how much spread private credit can generate, but how flexibly capital can be allocated, reallocated, and, when needed, released over time without impairing long term returns.

This shift is driving the emergence of a new generation of institutional evergreen private credit funds, designed to keep capital fully deployed across cycles, with clearly defined pathways for capital recycling and investor exit. While much market commentary has focused on ‘semi-liquid’ vehicles targeting private wealth, many GPs are developing private credit evergreen funds specifically tailored for institutional investors. This new wave of innovation has the potential to reshape the private capital landscape, permanently.

Defining the evergreen funds spectrum: introducing ‘run-off’ and ‘rolling vintage’ models

Evergreen private credit is often discussed as a single category. In reality, it encompasses structurally distinct models with materially different economic and liquidity outcomes. Three models dominate today’s market:

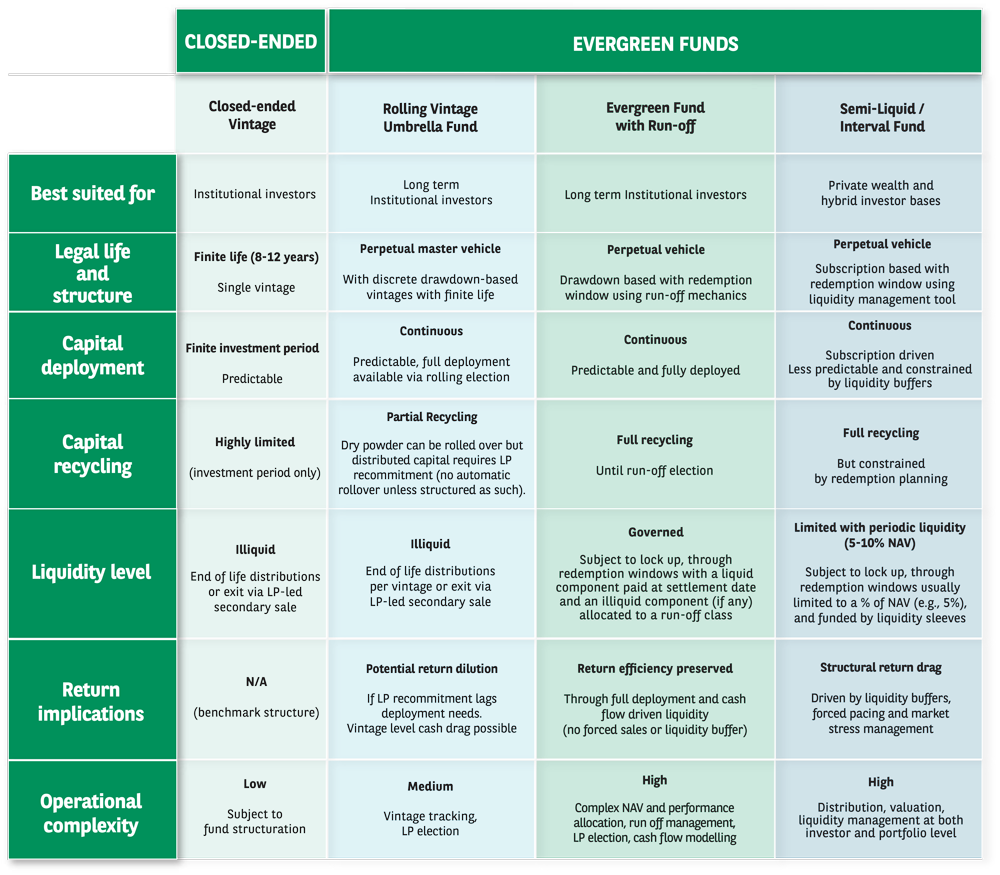

Semi-liquid evergreen funds

- Primarily designed to broaden access to private markets by offering periodic subscriptions and redemptions at NAV, typically within predefined liquidity windows.

- They appeal to private wealth investors and hybrid investor bases seeking exposure to private credit with enhanced accessibility, simplified onboarding and a familiar open-ended fund experience.

- To accommodate redemption activity, semi-liquid structures rely on liquidity management tools such as gates, notice periods, asset rotation or liquidity buffers. While these mechanisms provide optional liquidity, they introduce structural trade-offs between accessibility, portfolio construction and long-term capital deployment—particularly in credit strategies where full investment and carry compounding are critical to performance.

In contrast, institutional drawdown-based evergreen structures are based on a different premise. They are purpose-built for investors with long-duration capital, allowing portfolios to remain fully invested while introducing governance mechanisms for capital recycling and release.

‘Run-off’ evergreen funds:

- Designed for sophisticated institutional and professional investors seeking long-duration exposure. Investors may:

- Add commitment on a continuous basis, with capital drawn periodically at NAV, deployed into a diversified private credit portfolio and recycled into new investments.

- Receive income through periodic distributions or elect to reinvest cash flows within the fund.

- Submit redemption requests, though these requests do not trigger immediate liquidity. Crucially, investor exits are not met through redemption queues, or discretionary liquidity windows.

- Upon receiving a redemption request, the GP first assesses the portion of liquidity that can be met organically through portfolio income, loan repayments, and other recurring cash inflows. In parallel, the GP evaluates the availability of undrawn commitments that can be deployed. Together, these two levers determine the share of an exit that can be satisfied on a liquid basis. The illiquid portion is instead allocated to a dedicated run-off class, which receives an allocation of the fund’s portfolio at redemption NAV date and is no longer exposed to new investments.

- This framework ensures liquidity is provided in a deliberate and disciplined manner, aligned with the underlying cash-flow profile of the portfolio, while protecting remaining investors from forced asset sales and preserving long-term capital efficiency.

‘Rolling vintage’ umbrella funds:

Also designed for sophisticated institutional and professional investors, these vehicles are:

- Typically structured as umbrella funds—such as SICAV RAIFs in Luxembourg or ICAVs in Ireland. Each sub-fund represents a distinct vintage with its own fundraising period, capital call mechanics, and investment timeline.

- Each vintage mirrors a closed-ended fund, but with a critical feature controlled by the LP. At the end of the investment period, LPs elect whether to roll uncalled capital into the next vintage, with no GP discretion.

- Distributed capital is not automatically reinvested: LPs must actively recommit (though some newer structures now offer auto-roll options for distributed proceeds).

Evergreen private capital structures vs closed-ended structures: A comparison

VIEW FROM APAC

The evergreen model is evolving from a niche alternative to a core strategic pillar for sophisticated APAC allocators and managers. It represents a maturation of the region’s private markets, aligning investor and manager interests over the long term.

Private credit activity is concentrated in Singapore, Australia, India, Japan and South Korea and select ASEAN economies, each supported by mature vehicles such as Singapore Variable Capital Companies (VCCs) and Australian Managed Investment Schemes (MIS) that can host perpetual vehicles. Consequently, the region has progressed from early exploration to full-scale implementation. GPs are actively shaping the evergreen landscape, through adapting the global model to incorporate features pioneered in APAC and investing further in the ecosystem by attracting expertise, capital and further accelerating development.

We see both established, large-scale GPs and smaller, credit and speciality finance managers entering this space. For example, we are working closely with a major global private debt manager to launch an APAC-focused evergreen vehicle. Leveraging its deep credit expertise and permanent capital structure, the fund will continuously deploy and recycle capital, giving institutional investors transparent, liquidity-controlled private credit returns. With the rapid growth of pension and sovereign wealth funds in APAC, as well as growing allocations from financial sponsors, family offices and ultra-high net worth investors, evergreen funds will continue to be a major lever for GPs to meet this demand.

Redefining the GP-LP relationship

These innovative ‘run-off’ and ‘rolling vintage’ evergreen funds offer a new paradigm in GP-LP relations.

For GPs, this LP-led discipline creates tangible structural advantages. GPs can develop longer-term partnerships with LPs through stable, sustained allocations. When structured effectively, these funds can lead to lower structural costs, as capital is compounded within a durable platform rather than repeatedly raised, deployed and wound down across successive vintages.

For LPs, evergreen funds simplify portfolio construction and operations. They enable streamlined due diligence, more predictable capital planning and allocation, and reduce the operational burden brought about by repeated commitments to closed-ended funds or AML-KYC onboardings.

This increased optionality, liquidity elections and capital recycling mechanisms can offer LPs more control and influence over their investments. But in order to deliver this, GPs need a servicing partner who can successfully manage the operational complexity and provide the robust infrastructure and expertise needed.

The operational backbone of institutional evergreen platforms

GPs will increasingly need to rely on specialist operational expertise, frameworks and technology to manage liquidity as well as incoming and outgoing investors. With the complex flow of capital for both models, GPs need an integrated banking and fund administration partner who can support them with five critical functions:

- Governance of investor-level allocations across vintages and run-off classes

Administration platforms must be able to dynamically recalibrate investor-level allocation keys across commitments, invested capital, NAV and segregated run-off exposures without manual intervention or operational break points. - Liquidity management support

Modelling and executing liquidity flows across portfolio income, repayments, new drawdowns and investor elections—without forced asset sales. - Run-off administration

Operationalisation of run-off classes through vertical accounting, P&L crystallisation and cash-flow segregation. - Bespoke performance fee calculation

Customised fee and carry calculations by vintage structures for rolling vintage and bespoke performance fees using high water mark and hurdle principles, aligned with long-term compounding dynamics. - Digital reporting and advanced analytics

GPs need granular, forward-looking reporting across vintages and investor profiles which can be increasingly enhanced by digital tools, workflows and AI-driven analytics.

Capturing the opportunity

As institutional investors prioritise balance sheet discipline over yield maximisation, run-off evergreen and rolling vintage structures are becoming a critical part of GPs’ toolkits. At BNP Paribas, we are working with several private managers across EMEA and APAC to support them in their evergreen fund launches. Such close and collaborative partnership between GPs and their banking and fund administration providers will be key to scaling up, and for GPs to truly deliver the promise of these new evergreen structures.

- 2015 figure: Pitchbook h1-2025-global-private-debt-report.pdf

2025 figure: AIMA Press Release: Strong growth sees private credit market reach US$3.5 trillion ↩︎